By Sandeep Vasudevan, Partner at Presciant, a Brand Strategy and Valuation Firm

Brand equals trust. And in agriculture, trust decides what gets planted. Agriculture brands are especially critical.

Yet the agriculture industry systematically undervalues the very asset its customers care about most. The global agriculture market was valued at $1.2 trillion in 2023. Its biggest players—Bayer Crop Science, Corteva, Syngenta, BASF, and FMC invest billions in R&D, but spend just 3–5% of revenue on sales and marketing. That compared to 10-15% in high-tech manufacturing or pharmaceuticals.

Presciant’s extensive global research across agriculture’s value chain—from growers in the American heartland to agronomists in Brazil, from dealer networks in Europe to emerging markets in Asia—reveals the core problem: Farmers value trust and relationships above product performance, yet companies measure and invest in exactly the opposite. What follows examines why this gap exists among agriculture brands, what it costs, and how forward-thinking players are closing it.

Agriculture’s Most Undervalued Asset: Brand = Trust

Agriculture is a “trust-first” category. When a grower selects a hybrid, a fungicide, or a digital platform, the results of that decision may not be known for an entire growing season. You can’t test-drive a corn hybrid or return a bad batch of seed. The purchase decision, then, is an act of faith.

Yet, despite this, ag marketing remains dominated by rational, functional messaging; Yield data, resistance claims, chemical formulations. Little effort goes into messaging around agriculture brands .

The irony? Agriculture brands function in one of the most emotional purchase categories on Earth.

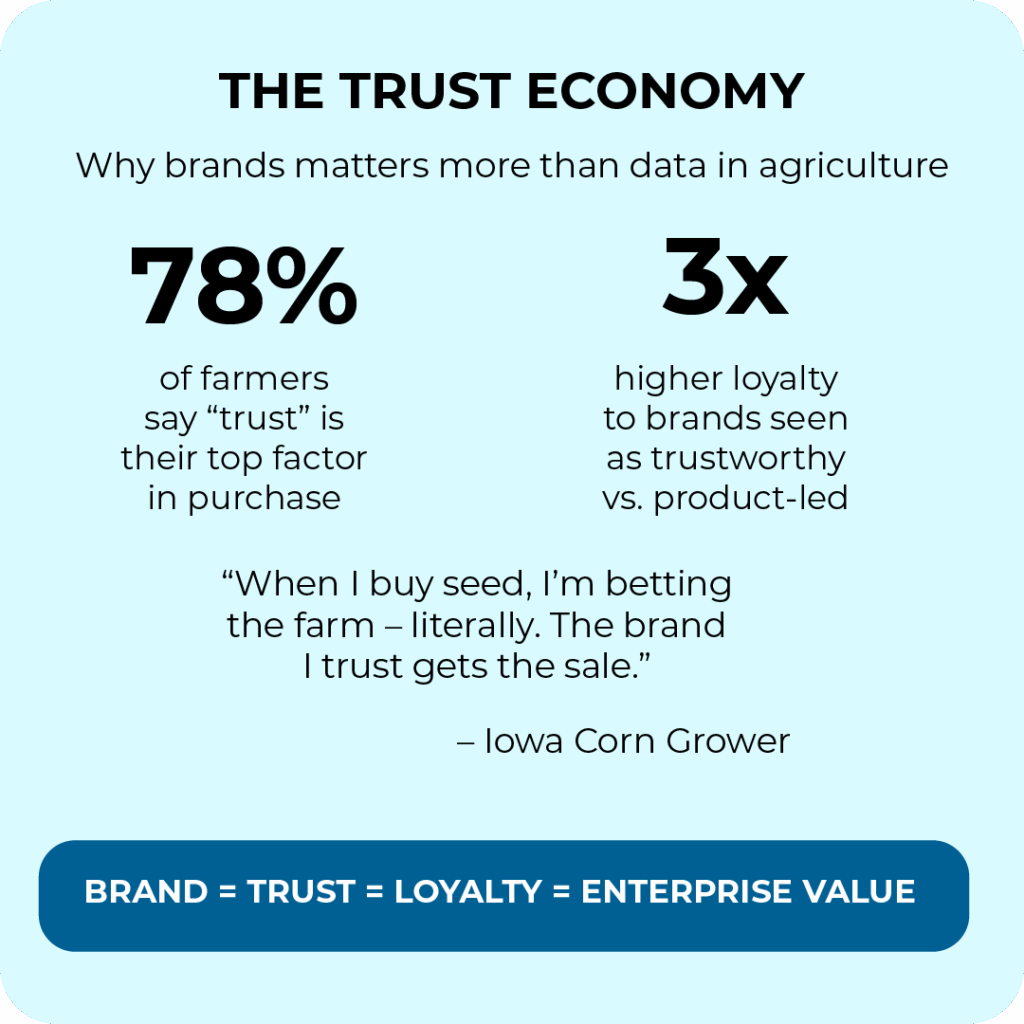

Here’s the gap in stark terms: 63% of farmers identify themselves as brand loyal, with some equipment manufacturers commanding loyalty rates exceeding 75%. Yet a 2024 Brand Finance Agriculture Sector Report found that only 12% of ag leaders consider brand equity a primary driver of competitive advantage.

Farmers don’t cite specs when explaining their loyalty. They cite peace of mind and familiarity. Among large-scale farmers, 98% say John Deere meets their expectations. One farmer described it perfectly: “It’s not a John Deere, and that’s just stupid” acknowledging that while a competitor’s tractor worked flawlessly, the emotional connection simply wasn’t there.

The tangible value is clear: A 2023 study by the Agri-Marketing Association found that companies scoring in the top quartile for customer-perceived ‘Trust & Integrity’ achieved 2.5x higher repeat purchase rates and could sustain an average 8% price premium over their nearest functional competitor. Meanwhile, brand-led companies in adjacent industries command up to 20–30% valuation premiums over product-led peers.

The uncomfortable truth: Agriculture is selling to some of the most brand-loyal customers on Earth while systematically undervaluing the very thing those customers care about most: their agriculture brands.

The Loyalty Trap: Misplaced Loyalty

Agriculture’s loyalty problem isn’t lack of loyalty. It’s that the loyalty lives in the wrong place. The purchase decision belongs to retailers, agronomists, and seed advisers who have direct relationships with growers, not to the company’s agriculture brand.

Seed companies acknowledge this reality: “The grower’s most important decision within that one cropping year is going to be the hybrid or variety they place on that acre. They need a trusted partner, their dealer that’s going to bring our technology to life on the farm.” Translation: The brand equity companies think they own is actually borrowed from their distribution partners.

Yet ag companies continue to organize around product brands, launching new herbicide sub-brands, seed line extensions, and digital platform logos rather than building the company brand that could create direct loyalty. They invest billions in R&D for better chemistry while the real influence over purchase decisions lives one layer removed.

This creates existential vulnerability. Dealer consolidation accelerates across the industry. When a trusted dealer retires, gets acquired, or switches manufacturer allegiances, companies discover their “loyal” farmers were loyal to a person, not a brand.

The hard truth: you can’t control loyalty you don’t own.

The House of Brands Problem: The Sprawl of Chemistry, Data, and Biology

The ag industry today is cluttered with sub-brands, hybrids, and heritage labels—hundreds of them. Companies like Bayer Crop Science, Corteva Agriscience, and BASF Agricultural Solutions operate as houses of brands. Legacy brand portfolios have been built by decades of mergers and acquisitions. Each new molecule or hybrid arrives with its own logo and claim.

Today, the agriculture product brand sprawl is compounded by AgTech M&A. Every major player now has an ecosystem of digital farming tools (e.g., Bayer’s Climate FieldView, Corteva’s Granular) and biological inputs (e.g., microbial seeds, bio-pesticides). Farmers are now dealing with a ‘House of Brands,’ not just for chemistry, but for data and biology, each requiring a separate login, training, and trust contract. Maintaining this vast, complex network of disconnected product brands costs an enormous amount in fragmented marketing spend, IT integration, and internal management, further diluting the master brand’s impact.

The result? A field of confusion.

Even seasoned agronomists struggle to articulate what distinguishes one herbicide or digital platform from another. A farmer once told us, “All these brands are like cousins in the same family. Different names, same DNA.”

In an age of shrinking marketing budgets, this agriculture product brand sprawl is unsustainable. Supporting dozens of disconnected agriculture brands is what fragments spend and dilutes impact. More critically, it obscures the one thing that could differentiate: why you exist beyond making better chemistry.

But here’s the twist: While Big Ag struggles with product brand name sprawl, direct-to-consumer agricultural sales are projected to grow by 25% in 2024, and smaller players are using brand clarity as a competitive weapon. Buyers are increasingly distrustful of mega-brand food conglomerates and seek alternatives to Big Agriculture, creating an opening for agriculture brands that can tell a coherent, authentic story.

Brand is important now and will get more so.

The shift is accelerated by the “Make America Healthy Again” movement and increased awareness among consumers about food sources. Independent farms that build strong local agriculture brand identities are capturing market share from established players who’ve let their brand architecture become Byzantine.

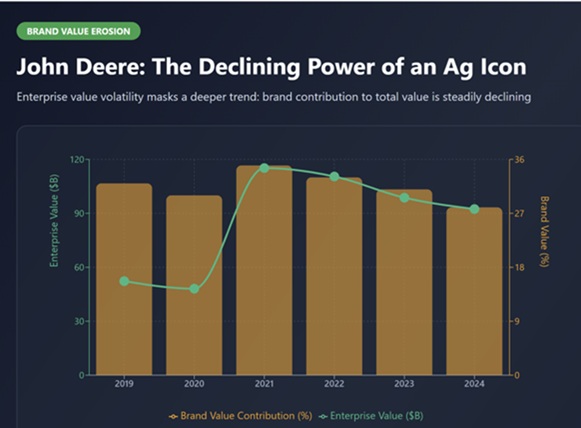

The Monsanto Shadow: A Masterclass in Brand Liability

Bayer’s $63 billion acquisition of Monsanto was one of the most consequential—and reputationally costly—deals in modern corporate history. The Monsanto brand, synonymous with innovation but dogged by controversy, was retired within months of the merger.

Bayer’s $63 billion acquisition of Monsanto was one of the most consequential—and reputationally costly—deals in modern corporate history. The Monsanto brand, synonymous with innovation but dogged by controversy, was retired within months of the merger.

To date, Bayer has paid over $10 billion to settle Roundup® litigation. The deal is now considered one of the worst corporate mergers in history, with Bayer’s market capitalization falling to roughly what the company paid for Monsanto alone. Using a brand valuation model, we can estimate the destruction of intangible brand equity for Monsanto/Roundup alone at well over $30 billion.

Yet five years later, Bayer still struggles to escape the shadow of this mistake. Despite the global phaseout of the Monsanto brand name, public sentiment data shows that over 60% of respondents still associate Bayer with GMOs and glyphosate litigation.

The lessons for agriculture brands are brutal:

- Due diligence failed to properly value reputational liabilities as financial liabilities. Public sentiment, scientific consensus, and judicial outcomes evolve and a brand can become a millstone around a company’s neck.

- You can’t acquire your way out of a brand problem. Bayer thought it was buying innovation and market position. What it actually bought was a cultural lightning rod and a litigation time bomb.

- In trust-first categories, negative brand equity doesn’t depreciate; it compounds. The agriculture industry’s long memory means that controversy sticks like glyphosate to leaves.

This case raises a hard question for the entire industry: Can agriculture brands win back trust without rebranding trust itself?

Seeds of Change: Farmers Are Buying Outcomes, Not Inputs

While legacy agriculture brands wrestle with their portfolios, a new crop of ag innovators is redefining what branding means in this sector and they’re doing it with a fraction of the resources.

Indigo Ag built its identity not on yield or inputs, but on a carbon-positive purpose. Rewarding farmers for sustainable practices. They understood that farmers increasingly see themselves as stewards, not just producers.

Pivot Bio positions itself as the “anti-fertilizer company,” using bold, insurgent messaging around microbial nitrogen. The brand is built on contrast, not comparison.

Bushel and FarmLogs use consumer-style UX and storytelling to make data “human.” They recognized that farmers were tired of enterprise software designed by people who’d never seen a combine tractor.

Even smaller seed companies like Beck’s Hybrids and Stine Seeds have leaned into authenticity and community, using the voice of the farmer in their branding. They’ve turned their regional scale into an advantage: “We’re not everywhere because we’re not for everyone.”

These agriculture brands understand something many incumbents do not: Farmers don’t want to buy more science. They want to buy confidence in their decisions

Marketing executives need to focus on building trust and authenticity through transparent communication, as younger generations are research-oriented and critical when they believe they’re being greenwashed. The story is becoming more important as consumers become more discerning and health-conscious.

Why Brand Architecture Is Now a Boardroom Issue

As Big Ag splits and reshapes itself. Corteva spinning off elements of itself into separate companies and Bayer Crop Science rumored to be considering the same, the industry is entering a period of identity flux.

As Big Ag splits and reshapes itself. Corteva spinning off elements of itself into separate companies and Bayer Crop Science rumored to be considering the same, the industry is entering a period of identity flux.

Each spin-off, merger, or rebrand is not merely a corporate exercise; it’s a chance to redefine who these companies are in the eyes of the world.

The key strategic question: “Is our current brand architecture (whether a House of Brands or a Branded House) optimized to maximize customer clarity and enterprise value?”

Shifting or optimizing architecture requires courage and clarity about where true equity resides and how to align it with future growth strategies.

Consider the timing: Net farm income is expected to fall to its lowest level in nearly a decade, with a forecasted decline of 15-20% from 2024 levels. Farmers are under unprecedented financial pressure. The answer isn’t volume, it’s generating and capturing greater value from the acre.

In this environment, agriculture brands become even more critical. When prices are compressed and commodities are down, the only way to command premium pricing is through branding. The only way to maintain loyalty when farmers are scrutinizing every dollar is through relationship equity that transcends transactions.

The Right-to-Repair Reckoning: When Control Becomes Poison

The fight over right-to-repair farm equipment isn’t about IP protection or service revenue; it’s a brand crisis disguised as a policy debate. Farmers aren’t just asking for technical access they’re asking for autonomy. For control.

The fight over right-to-repair farm equipment isn’t about IP protection or service revenue; it’s a brand crisis disguised as a policy debate. Farmers aren’t just asking for technical access they’re asking for autonomy. For control.

For farmers, the right-to-repair conflict is a crucible moment for the brand contract. A recent Farming News report noted that a single tractor error code requiring a dealership visit can result in 12–72 hours of downtime during a critical harvest period, a time cost that translates to tens of thousands of dollars in lost revenue and wasted labor.

When John Deere fights right-to-repair legislation, they’re creating a brand experience of unnecessary cost, frustration, and powerlessness. That message is “You don’t own this, you lease the privilege of our permission.” It is antithetical to the farmer’s identity of self-reliance and perseverance. Loyalty is an insurance policy, but when you test the limits of that loyalty long enough, you’ll find them.

The Harvest Ahead: Brand in the Age of ESG and Biologicals

Corporate agriculture brands are stuck in the past. True brand strategy is about the future.

Corporate agriculture brands are stuck in the past. True brand strategy is about the future.

The agriculture industry is undergoing a fundamental transformation, driven by biological innovation, precision agriculture, and stringent sustainability (ESG) demands. This rapid technological shift—evidenced by the skyrocketing adoption of Variable Rate Technology (VRT) for pesticide application from 20% in 2019 to over 50% in 2024—Is introducing unprecedented complexity and choice for the farmer. The core problem is that corporate agriculture brands are failing to translate this science into a clear, unified value proposition, remaining organized around the chemistries of the 1990s rather than the integrated outcomes of the future.

This agriculture brand failure carries a severe financial penalty, especially as the industry consolidates. The urgency for brand clarity is compounded by investor pressure and strategic imperatives like spin-offs and M&A. Investment banks increasingly use Brand Equity Scores as a proxy for the ‘sticky revenue’ and ‘future growth premium’ of a business unit. In the context of potential transactions, poor brand architecture the result of decades of neglect penalizes the enterprise value by creating complexity and obscuring the growth story for investors and acquirers.

The agriculture brands that will successfully navigate this new era are those that re-position from ‘input providers’ to ‘outcome partners.’ In this model, the brand promise isn’t just yield performance, but verifiable, sustainable value, value that satisfies the farmer’s balance sheet, meets corporate ESG standards, and protects the planet. Brand becomes the necessary translation layer between complex science and trusted, measurable results.

What Every Ag Company Should Be Asking Itself (The Boardroom Checklist)

Here is the uncomfortable brand checklist that most ag players avoid. These are the strategic questions that turn brand awareness into enterprise value:

On Emotional Equity:

- What emotional space do we own in the farmer’s mind beyond performance?

- When farmers think of us, do they feel something or just recognize something?

- Are we building believers or just customers?

On Brand Architecture:

- How does our master brand show up across categories; seed, crop protection, digital, and biologicals?

- Do farmers understand what we stand for, or just what we sell?

- Is our brand structure optimized for the portfolio we have, or the one we had a decade ago?

On Portfolio Rationalization:

- Which of our product brands actually drive purchase versus fragment our equity?

- How many of our sub-brands could disappear tomorrow without affecting revenue?

- Are we funding confusion? Are we wasting money by supporting too many brands? Are our marketing dollars being put to use in the most effective way?

On Valuation and Measurement:

- Can you measure the returns from your marketing investment?

- Do we track brand health with the same rigor we track yield data?

- Are we using brand valuation as a strategic tool to grow value? or a vanity exercise?

On Ecosystem Loyalty:

- Are customers loyal to our company, or are they loyal to our dealers, or to our agronomists? And does it matter?

- Do we lose our customers if our dealer network gets acquired?

- Are we investing in the relationships that actually drive purchase decisions?

Key Takeaway: Loyalty’s Expiration Date

Brands are the most undervalued crop in modern agriculture.

Agriculture has coasted on inherited loyalty for decades, loyalty built when dealers were neighbors and choices were few. That world is disappearing. Dealers are consolidating. Younger farmers are more willing to try new brands

Farmers cite dealer relationships as the most important factor in loyalty, with 3 of the top 5 switching factors tied directly to dealer performance. What happens when the dealer who knew your grandfather retires and is replaced by a regional manager optimizing for EBITDA?

Those who plant their agriculture brand early and nurture it with purpose, consistency, and clarity will own the next harvest of trust, loyalty, and enterprise value.

Those who don’t will discover, too late, that loyalty has an expiration date. And in agriculture, once the ground goes fallow, it takes a generation to make it fertile again. The question isn’t whether agriculture needs stronger brands. The question is whether ag companies will build them before the loyalty they’ve inherited runs out.